Click to see the full-size ad.

Click to see the full-size ad.

Click to see the whole magazine.

Click to see the whole magazine.

Skip to Main Content

Company News

Carrington is on the June 2018 cover of the Scotsman Guide

Pricing Improvement on Near-Prime and Non-Prime Loans

Effective May 30, 2018, Carrington Mortgage Services, LLC (CMS) will offer improved loan level pricing for the Near-Prime and Non-Prime Loan programs. The matrices below list the amounts of the applicable Loan Level Price Adjustment improvements by FICO and LTV. Refer to the CMS Rate Sheets for the latest pricing.

Near Prime

Non-Prime

[btn link="https://carringtonhomeloans.com/drop-in/CMSWholesaleRates.pdf" color="crimson" size="size-m"]View Today's Rates[/btn]

Not an approved Carrington broker?

[btn link="/become-approved/" color="crimson" size="size-m"]Get Approved[/btn]

Housing Starts Stutter

Last Week in Review:

Housing Starts stall in April, while registers were ringing at retailers.

Retail Sales rose 0.3 percent from March to April, the Commerce Department reported, with sales highest at furniture stores, clothing stores and gasoline stations. On a year-over-year basis, Retail Sales jumped a solid 4.7 percent. The Retail Sales report is a measure of the total receipts of retail stores from samples representing all sizes and kinds of businesses throughout the nation, making it a key indicator regarding the state of our economy.

Home construction was a different story in April, however. Construction on new homes declined in April from March due in part to a rise in the price of lumber. April Housing Starts fell 3.7 percent from March to an annual rate of 1.287 million units, below expectations. Single-family home starts, which make up a big chunk of residential construction, rose 0.1 percent from March to April, while multi-dwelling starts of five or more units fell 12.6 percent. On a positive note, Housing Starts were up 10.5 percent from April 2017.

Building Permits, a sign of future construction, fell 1.8 percent from March to an annual rate of 1.352 million units. National Association of Home Builders Chairman Randy Noel explained, "The record-high cost of lumber is hurting builders' bottom lines and making it more difficult to produce competitively priced houses for newcomers to the market."

Mortgage Bonds struggled in the latest week, falling below a key technical level and hitting seven-year lows. Home loan rates are tied to Mortgage Bonds and, as a result, rates hit seven-year highs. However, rates remain attractive on a historical basis.

Memorial Day 2018 Holiday Lock Desk Hours

The Lock Desk will be closed on Monday, May 28, 2018 for Memorial Day, which is a Federal Holiday. Normal lock hours will resume on Tuesday, May 29, 2018.

Additionally, the Lock Desk will close early on Friday, May 25, 2018 at 10:00 A.M. PST due to the early close of the financial markets.

Locks that expire on the holiday will automatically roll to the next business day. In addition there are some important disclosure considerations associated with the holiday:

- Monday, May 28, 2018 cannot be included in the rescission period for refinance transactions.

- Monday, May 28, 2018 cannot be included in the seven (7) business day waiting period between the date the initial Loan Estimate (LE) was provided to the borrower and the consummation of the loan

- When re-disclosure of the LE is required, Monday, May 28, 2018 cannot be included in the four (4) business day waiting period between the date the revised LE was provided to the borrower and the consummation of the loan.

- When re-disclosure of the CD is required, Monday, May 28, 2018 cannot be included in the three (3) business day waiting period between the date the revised CD was provided to the borrower and the consummation of the loan.

Issues related to locks should be sent via email to lockdesk@carringtonms.com.

Consumer Inflation Below Expectations

Last Week in Review:

Consumer and wholesale inflation were tame in April, while geopolitical events also made headlines.

The Consumer Price Index (CPI) rose 0.2 percent in April, just below expectations, the Bureau of Labor Statistics reported. This was down from the 2018 high of 0.5 percent recorded in January. The numbers revealed an uptick in energy and food prices which was offset by a decline in demand for used cars and trucks. The Core CPI, which strips out volatile food and energy prices, rose 0.1 percent, also below expectations.

Inflation at the wholesale level was also tame in April as the Producer Price Index (PPI) rose 0.1 percent. Core PPI rose 0.2 percent, as expected.

Tame inflation is typically good for Mortgage Bonds, as well as the home loan rates tied to them, because inflation reduces the value of fixed investments like Bonds. And Mortgage Bonds were boosted by the tame inflation data in the latest week.

It's also important to remember that many factors impact both Stocks and Bonds. Strong economic news can benefit Stocks (sometimes at the expense of Bonds), while geopolitical turmoil can have the opposite effect. Stocks received a boost in the latest week when energy Stocks lifted the entire market, as oil prices spiked after President Trump announced his decision to withdraw from the Iran nuclear deal. The release of prisoners from North Korea and the scheduling of a meeting between President Trump and Kim Jong-un also lifted some uncertainty and helped the recent rise in Stock prices.

Investors will be watching headlines from the Middle East and Korea closely in the coming weeks as they decide where to put their investing dollars.

For now, though, home loan rates have trended higher this year, they remain attractive and near historically low levels.

If you or someone you know has any questions about home loans, please contact us. We'd be happy to help.

Jobs, Inflation and the Fed

Last Week in Review:

The April Jobs Report disappointed while inflation ticked up in March. Plus, the Fed met.

The Jobs Report for April was a bit of a disappointment, as job creation rose from March but came in below expectations. There were 164,000 new jobs added in April, below the 190,000 expected, the Bureau of Labor Statistics reported. This was up, however, from the 135,000 recorded in March (which was revised higher from 103,000). The Unemployment Rate fell to an 18-year low of 3.9 percent. Wage growth fell to 2.6 percent on an annual basis, down from the 2.9 percent recorded in January. Month-over-month hourly earnings rose 0.1 percent versus the 0.2 percent expected.

The Fed's favorite inflation measure, annual Core Personal Consumption Expenditures (PCE), showed that inflation rose 1.9 percent in the 12 months through March. This was up from the 1.6 percent annual increase recorded in February. The Core reading excludes volatile food and energy prices. March's number was the biggest increase since February 2017, and it brings annual Core PCE closer to the Fed's target of 2.0 percent.

Inflation reduces the value of fixed investments, like Mortgage Bonds, meaning inflation can hurt Mortgage Bonds and the home loan rates tied to them. It will be important to see if signs of inflation remain in the air.

The Fed met and, as expected, left its benchmark Fed Funds Rate unchanged at 1.5 to 1.75 percent. This is the rate at which banks lend money to each other overnight, and it is not directly tied to home loan rates. The Fed noted, as mentioned above, that inflation has moved closer to its 2.0 percent target, employment growth has been strong, and that the economy is growing at a moderate rate.

Over in the housing sector, high demand plus a limited supply of homes for sale on the market pushed home prices higher in March. Research firm CoreLogic reported that home prices, including distressed sales, rose 7 percent from March 2017 to March 2018, while there was a 1.4 percent gain from February to March. Looking ahead, CoreLogic forecasts a 5.2 percent rise in home prices from March 2018 to March 2019.

Despite the warm inflation reading, the disappointing labor market news in part helped Mortgage Bonds bounce off five-year lows. Home loan rates improved this week and remain historically attractive.

If you or someone you know has any questions about rates or home loans, please get in touch. We'd be happy to help.

Introducing a new Near-Prime Product

Overview

Effective May 3, 2018 Carrington Mortgage Services, LLC (CMS) will introduce a new Near-Prime Product to broaden our commitment to serving the underserved borrower!

The Near-Prime product is well suited for borrowers who may have credit challenges but need pricing that is closer to prime rates. The program features Fixed and Adjustable Rate loan programs with FICO scores down to 620.

General Highlights

- Recent Mortgage / Rental Lates up to 1 x 30 x 12

- Foreclosure, Short Sale, Deed in Lieu and Bankruptcy with 36-month seasoning

- Max Debt Ratios from 50% up to 55%

- First Time Home Buyers allowed

- Non-warrantable Condo Permitted (max 80% LTV)

- Fully Documented Loans, 24 Months Bank Statements, 12 Month Bank Statements, and 1-Year Alternative Documentation

- No Mortgage Insurance required

- No Prepayment Penalties

Near-Prime Program Terms

- Purchase, Rate/Term and Cash-Out Transactions (up to $500,000 cash-out)

- 30 Year Fixed, 5/1 and 7/1 LIBOR ARMs

- Maximum Loan Amount to $1.5MM

- Cash-Out available to $500K

- Primary Residence and Second Homes

- Max LTV/CLTV: Up to 95%*

- Min FICO: 620

- Not Available in AK; MA; WV

*Refer to the CMS Near-Prime Matrix for LTV requirements.

Home Sales Rise, Inventory Still Lean

Last Week in Review:

Home sales increased in March, though inventory remains a challenge. First quarter GDP fell but beat expectations.

March Existing Home Sales rose 1.1 percent from February to an annual rate of 5.60 million units, the National Association of REALTORS® reported. However, sales were down 1.2 percent from March 2017 due in part to continued low inventories and affordability issues. March saw just a 3.6-month supply of existing homes for sale on the market, well below the 6-month level that is considered healthy.

Inventory of new homes for sale on the market fared better in March, with a 5.2-month supply of homes available. March New Home Sales rose 4 percent from February to an annual rate of 694,000, a four-month high, per the Commerce Department. Sales also were up 8.8 percent from March 2017. However, there were considerable differences in sales around the country. In the Northeast, sales plunged 54.8 percent, while sales in the West soared to their highest level since December 2006, up 28.3 percent.

Home prices also continued to rise, as the February S&P/Case-Shiller 20-City Home Price Index showed that home prices rose 6.8 percent from February 2017.

Finally, the Bureau of Economic Analysis reported that economic growth in the first quarter of 2018 slipped from the final three months of 2017, though the number did beat estimates. The first reading on first quarter Gross Domestic Product (GDP) showed a gain of 2.3 percent, down from the 2.9 percent recorded in the previous quarter, but above the 2.1 percent expected. GDP is the monetary value of finished goods and services produced within a country's borders in a specific time period. It is considered the broadest measure of economic activity.

Mortgage Bonds bounced higher in recent days after declining over the last few weeks. Home loan rates remain historically attractive.

If you or someone you know has any questions about rates or home loans, please get in touch. We'd be happy to help.

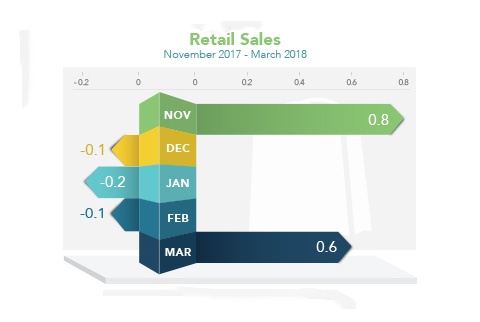

Housing Starts, Retail Sales Rise

Last Week in Review:

Retail Sales and Housing Starts blossom in March.

Retail Sales rose 0.6 percent in March, above the 0.4 percent expected and up from the decline of 0.1 percent in February, the Commerce Department reported. Leading the boost was spending on automobiles and health and personal care items. Consumer spending makes up two-thirds of U.S. economic activity and is crucial to a healthy economy.

Housing Starts also bloomed in March, rising 1.9 percent from February to an annual rate of 1.319 million units, per the Commerce Department. February's figure was also revised higher to 1.295 million units. Housing Starts got a big boost from a 16.1 percent monthly increase from the multi-dwelling sector. However, things were less rosy for those interested in single family homes, as single-family starts fell 3.7 percent from February. From March 2017 to March 2018, Housing Starts were up 10.9 percent.

Building Permits, a sign of future construction, rose 2.5 percent from February to March to an annual rate of 1.354 million. Limited inventory remains a challenge in many areas of the country, so it will be important to see if Housing Starts continue to blossom and if single family starts shift gears higher.

Mortgage Bonds struggled in the latest week, approaching five-year lows, due to strong economic news and positive data. Home loan rates have edged higher but still remain historically attractive.

If you or someone you know has any questions about rates or home loans, please get in touch. We'd be happy to help.

Consumer Inflation Remains Tame

Last Week in Review:

Inflation remained tame in March, though the Fed still expects it to rise this year.

The Consumer Price Index (CPI) fell 0.1 percent in March, below the expected gain of 0.1 percent, the Bureau of Labor Statistics reported. Lower gas prices at the pump were to blame for the first decline in 10 months. When stripping out volatile food and energy prices, Core CPI was in line with expectations at 0.2 percent. However, Core CPI rose 2.1 percent on an annual basis, a 12-month high.

Inflation at the wholesale level was a bit hotter than expected, as the Producer Price Index (PPI) and Core PPI both rose 0.3 percent in March, versus the 0.2 percent expected.

Though inflation remained tame in March, the minutes from the Fed's March meeting showed that the Fed still expects inflation to rise this year. Inflation hurts the value of fixed investments like Mortgage Bonds, meaning a rise in inflation can cause Bonds to worsen. Home loan rates are tied to Mortgage Bonds, so a rise in inflation can cause rates to rise as well.

Geopolitical headlines also garnered attention in the latest week, as heightened tensions over Syria between the U.S. and Russia helped Bonds benefit temporarily from safe-haven trading. Earnings season also began and there is a growing sense that corporate earnings for the first quarter could be strong due to the tax cuts. This could benefit Stocks at the expense of Mortgage Bonds and home loan rates.

For now, Mortgage Bonds are trapped in a sideways trading pattern that began in mid-February. Home loan rates remain just above all-time lows.

If you or someone you know has any questions about rates or home loans, please get in touch. We'd be happy to help.